Home-equity borrowing stayed muted in the third quarter, Calculated Risk says

Federal Reserve data showed mortgage debt rose $108 billion in Q3 2025, matching Q2, while Calculated Risk said equity extraction remained limited.

By Maya Okafor · Markets Writer

· 3 min read

Homeowners were still not using their houses like easy cash machines in the third quarter, according to Calculated Risk. For everyday investors, that matters because housing debt can feed consumer spending in good times and deepen stress when home prices fall.

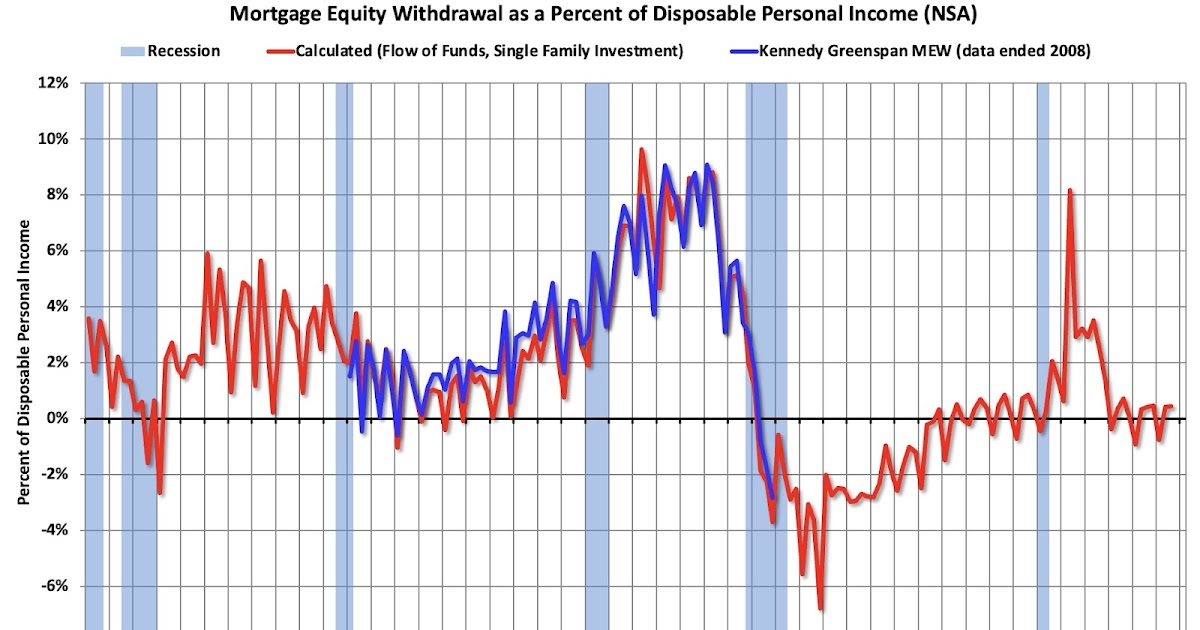

Calculated Risk, the real estate analysis site run by Bill McBride, pointed to the Federal Reserve’s Financial Accounts of the United States, also known as the Z.1 or Flow of Funds report, released Jan. 9. The Fed data showed mortgage debt rose by $108 billion in the third quarter of 2025, the same increase recorded in the second quarter.

Mortgage debt is the total amount households owe on home loans. A quarterly increase can come from several places: buyers taking out loans to purchase homes, owners refinancing, or owners borrowing against the value of homes they already own.

Calculated Risk’s focus was mortgage equity withdrawal, often shortened to MEW. That means homeowners pulling cash out of home equity, usually through refinancing or home-equity loans, rather than borrowing to buy a newly built home or an existing property.

Why the “home ATM” comparison matters

Calculated Risk said that during the mid-2000s housing bubble, many homeowners borrowed heavily against the equity they believed they had built up. The site said that behavior was jokingly described as using the home as an ATM.

That borrowing became a problem when home prices declined, according to Calculated Risk, because many owners ended up owing more than their homes were worth. That condition is called negative equity. It can make it harder for owners to sell, refinance, or absorb financial shocks.

The Fed’s long-term data also shows a sharp rise in mortgage debt during the housing bubble period, Calculated Risk said. After the bust, mortgage debt declined for nearly seven years as distressed sales, including foreclosures and short sales, erased a meaningful amount of debt.

Not all new mortgage debt is cash-out borrowing

Calculated Risk cautioned that the $108 billion increase in the third quarter should not be read entirely as homeowners taking cash out. Some of the increase reflects borrowing tied to adding to the housing stock, such as purchases of new homes.

That distinction is important for investors reading housing data. Debt used to buy newly built homes can support construction activity and housing supply. Debt used mainly to extract cash from existing homes can point more directly to household spending fueled by rising home values.

Calculated Risk’s takeaway was that the “home ATM” was mostly closed in the third quarter. The Fed data showed mortgage debt was still growing, but the analysis argued that the kind of broad equity extraction seen during the housing bubble was not the main story.

This story draws on original reporting from Calculated Risk.