Retirement stock-heavy portfolios draw fresh scrutiny after bond debate

A Wealth of Common Sense says 90/10 portfolios can work for some retirees, but bear-market timing can make the trade-off costly.

By Sofia Marchetti · Columnist

· 3 min read

A new retirement debate is putting the old 60/40 portfolio back under the microscope for investors who rely on their savings. A Wealth of Common Sense, responding to a reader question about a Wall Street Journal opinion piece by Mr. Posen, argued that a stock-heavy portfolio can build more wealth over time, but retirees need to understand the risk of selling during a long market decline.

The question came from a retired couple in their early 70s who said they hold an 80/20 mix of stocks and cash, with no bonds. They asked about Mr. Posen’s argument that many households may be holding too much in bonds.

According to the Wall Street Journal passage cited by the reader, Mr. Posen said some retirees should hold more high-quality bonds, especially if they need investment income or might have to sell assets to cover expenses in a bad year. But he said that may not apply to two large groups: the six million to seven million Americans with at least $1 million in investable assets, and households with more than $100,000 in investable assets whose noninvestment income covers their living costs.

The trade-off behind 90/10

A 60/40 portfolio usually means 60% stocks and 40% bonds. A 90/10 portfolio means 90% stocks and 10% bonds or cash. The appeal is straightforward: stocks have historically delivered stronger long-term returns than bonds, so a higher stock allocation can leave investors with more money if they can stay invested through downturns.

A Wealth of Common Sense said that logic is reasonable in many cases, but the timing risk is different in retirement. Workers who are still saving can keep buying during sell-offs. Retirees often need to withdraw from the same portfolio that is falling, which can lock in losses and leave fewer shares available for a recovery.

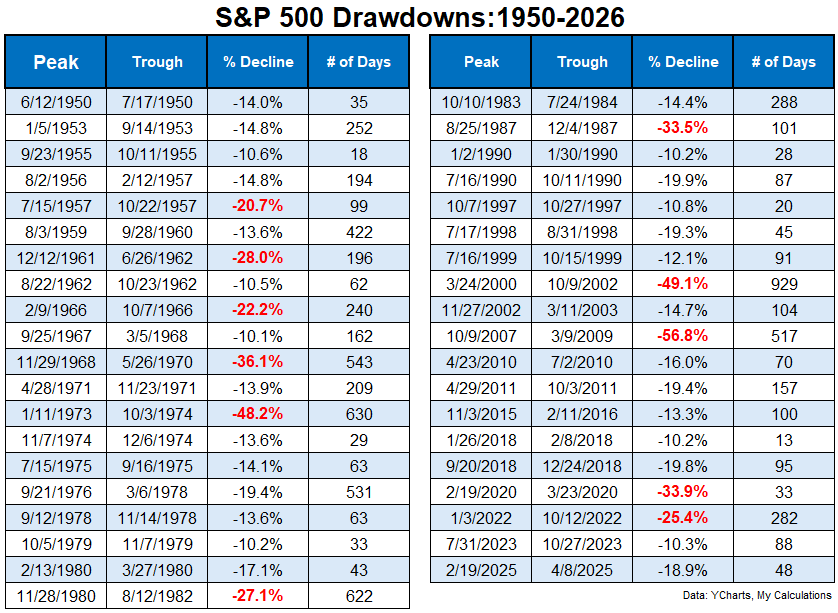

The post said the S&P 500 has had 39 double-digit corrections since 1950, or roughly one every two years on average. In those episodes, the average decline was 20%, and the average drop from market peak to low point lasted 193 days, according to the analysis.

The recovery period matters too. A Wealth of Common Sense said the average time to return to breakeven after those corrections was 306 days. Added together, the average investor spent close to 500 days below the prior high. The analysis noted that the figures used price-only data, meaning dividends were excluded, so total-return results would reduce the recovery time somewhat.

Bear markets change the math

Regular corrections are only part of the concern. A Wealth of Common Sense pointed to several longer bear markets, a term usually used for a decline of 20% or more from a recent high.

After the 1973-74 bear market, the post said it took almost six years for the market to return to breakeven. The dot-com bust took four and a half years to recover from the bottom. After the Great Financial Crisis, the S&P 500 peaked in fall 2007 and did not reach new highs again until 2013, according to the post. The Covid crash was much faster, recovering in less than 150 days.

The takeaway from A Wealth of Common Sense was not that retirees should avoid stocks. The post said retirees may need more equity exposure than traditional textbook models suggest because retirement can last 20 to 30 years and inflation can erode purchasing power.

Still, the analysis said retirees considering a 90/10-style allocation need a clear handle on spending and a backup plan for severe downturns. If the 10% cash or money-market sleeve is spent down during a bear market, rebuilding it may require selling stocks after they have fallen.

This story draws on original reporting from A Wealth of Common Sense.