Millionaire counts rise, but home equity changes the picture

Capgemini, UBS and Bloomberg data show more U.S. millionaires, with liquid wealth and housing wealth producing very different totals.

By Priya Nair · Economy Reporter

· 3 min read

The millionaire club kept growing in 2025, but the definition matters for investors reading wealth headlines. A count based only on investable assets gives a much smaller U.S. total than one that includes home equity, which is why estimates range from 8.73 million people to about 24 million households.

CNBC, citing Capgemini’s 2026 wealth report, reported that the global population of millionaires rose 7.9% to 25.3 million in 2025. Capgemini counted people with at least $1 million in liquid net worth, meaning wealth in assets that can be invested or sold more readily, excluding the value of a primary home.

That distinction is central. According to the Capgemini figures cited by CNBC, the U.S. added 730,000 new millionaires in 2025, bringing its total millionaire population to 8.73 million under the liquid-wealth definition.

Housing changes the math. A Wealth of Common Sense noted that Americans hold about $35 trillion in home equity. When home wealth is included, the U.S. millionaire count rises from around 9 million to roughly 24 million, according to the same analysis.

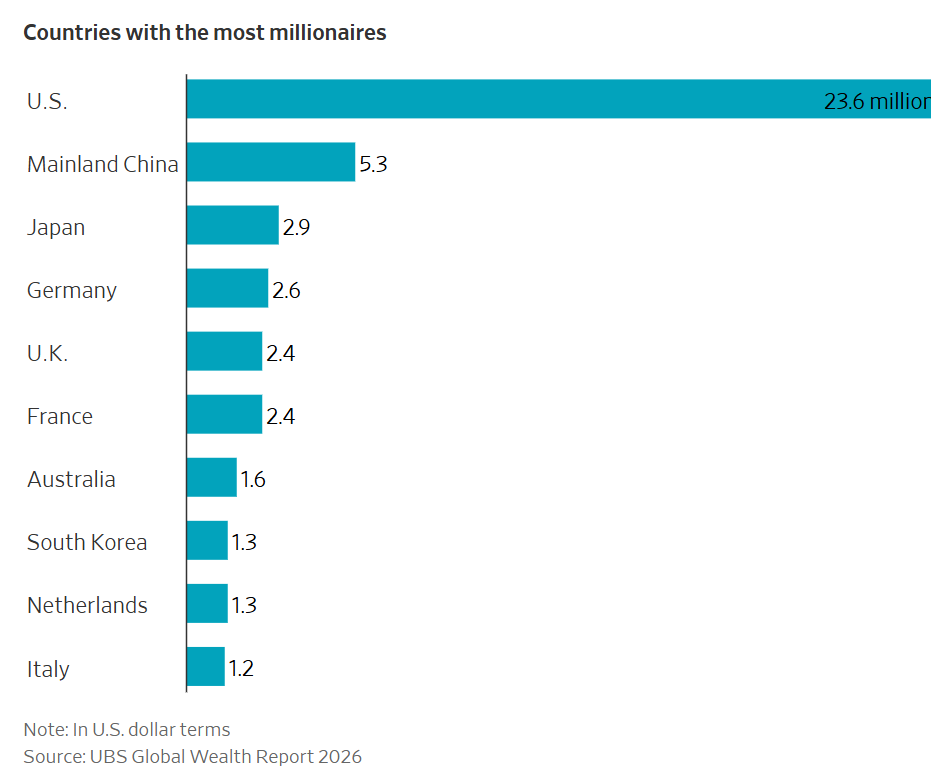

The Wall Street Journal, using UBS data, reported that the U.S. has nearly 24 million millionaire households, the largest total of any country. The Journal also reported that more than 440,000 people in the U.S., or over 1,200 per day, became millionaires in 2025.

Wealth is also concentrated among the very rich

The millionaire label covers a wide range of balance sheets. CNBC reported, citing Capgemini, that ultra-high-net-worth individuals, defined as people with $30 million or more, make up 1% of the millionaire population while holding 35% of millionaire wealth.

The Wall Street Journal also reported that the number of ultrawealthy people has grown considerably in recent years. Separately, the Journal said the fastest-growing global wealth segment over the past five years was people with $50 million to $100 million, which rose at a 7.3% pace.

Bloomberg data cited by A Wealth of Common Sense also put the number of U.S. millionaire households at about 24 million, or roughly 1 in 5 households. According to that report, one-third of those millionaire households reached that level within the past eight years.

Does $1 million still mean rich?

A Wealth of Common Sense framed the answer as context-dependent. The analysis said $1 million in liquid net worth would place someone in the top 1% globally and around the 88th percentile of American households.

Location is one factor. A dollar amount stretches differently in a lower-cost city than in Manhattan or San Francisco. Age also matters: reaching $1 million in a person’s 40s has a different financial meaning than reaching it in their 60s.

Spending is another key variable. In The Algebra of Happiness, Scott Galloway defines being rich as having passive income, such as dividends, pensions or Social Security, that exceeds annual spending. A Wealth of Common Sense highlighted that idea to show why lifestyle costs can matter as much as a headline net-worth number.

The takeaway for investors is that “millionaire” is a moving target. Liquid assets, home equity, cost of living, age and spending habits can all change what the same $1 million figure means in real life.

This story draws on original reporting from A Wealth of Common Sense.