U.S. stock data shows why average returns hide bumpy paths

Of Dollars and Data found U.S. stocks often beat their long-run average over one-year spans, while bad entry points still hurt.

By Priya Nair · Economy Reporter

· 3 min read

A century of U.S. market history shows why the familiar 7% real return figure can mislead investors who are thinking in months or years. An Of Dollars and Data analysis of U.S. stock returns from 1926 through 2025 found that outcomes varied widely across time frames, even though long-run results were strongly positive.

The analysis looked at real total returns, meaning stock returns that include reinvested dividends and are adjusted for inflation. That distinction matters for everyday investors because inflation reduces purchasing power, while reinvested dividends add to the amount compounding over time.

According to Of Dollars and Data, U.S. stocks have delivered about 7% a year after inflation and dividends over the very long run going back to 1871. But across one-year periods from 1926 to 2025, the expected return was higher: 9.15%.

The gap comes from the difference between an arithmetic average and a compounded return. An arithmetic average adds individual returns and divides by the number of periods. A compounded return shows what actually happens to money over time. Losses weigh heavily on compounding: a 50% gain followed by a 50% loss leaves an investor down 25%, even though the average of those two yearly returns is zero.

The one-year data also showed how uneven the ride can be. Of Dollars and Data found a 47% chance that a one-year U.S. stock return exceeded 10%, and a 26% chance that it topped 20%. The downside was real too: the analysis found a 17% chance of losing at least 10% over a one-year period.

Shorter windows looked much noisier. The expected return over one month was 0.68%, while the expected return over three months was 2.17%, according to the analysis. In both cases, the distribution of outcomes was broad, meaning the actual return in any given period could land far away from the average.

Longer holding periods showed fewer negative outcomes in the historical record. For five-year spans, Of Dollars and Data found that U.S. stocks returned more than 12% annualized in 26% of periods, while returns were below negative 4% annualized in 10% of periods. Annualized means the multi-year return is converted into an average yearly rate.

Across 10-year periods, the analysis found a 13% probability of any negative annualized real return. The expected annualized return was 7.03%, which Of Dollars and Data said was enough for money to roughly double over a decade.

Over 20-year periods, the annualized return slipped slightly to 6.93%, equal to about 3.8 times the starting investment across two decades, according to the analysis. In the 1926 to 2025 period, Of Dollars and Data found no 20-year span with a negative real total return. Looking further back to 1871, the analysis identified one such period: June 1901 through May 1921.

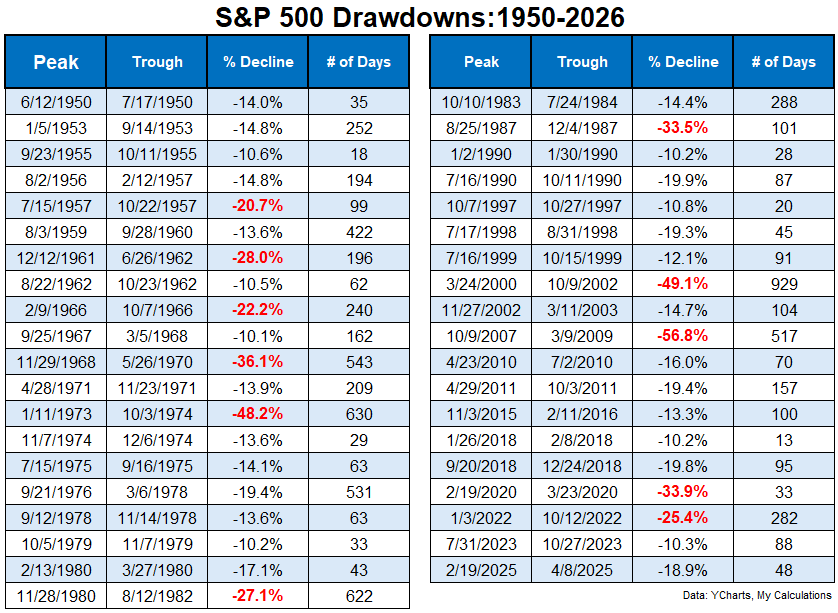

The author also compared U.S. history with other markets to show that long droughts are possible. Japanese stocks peaked in 1989 and did not reach new all-time highs until 2024, according to the analysis. Greek stocks remain more than 50% below their 1999 peak.

Of Dollars and Data also examined four difficult moments to begin investing in U.S. stocks: September 1929, January 1973, March 2000 and October 2007. In those cases, early losses were severe. The 1929 investor saw $1 fall below $0.25, while the 2007 investor lost half within 18 months. The 1973 and 2000 entry points did not recover for more than a decade.

Still, the historical record showed eventual recovery in the completed 20-year windows. After one year, all four entry points were negative, with losses from 19% to 38%. Five-year returns were negative in every case, and most 10-year returns were also negative. By 20 years, the periods with enough available history had positive real returns, according to Of Dollars and Data.

This story draws on original reporting from Of Dollars and Data.