Stock dominance raises new questions for households and policymakers

U.S. households have a larger share of wealth in equities, sharpening debate over whether stocks now shape retirement and policy choices.

By Sofia Marchetti · Columnist

· 3 min read

Stocks have become a bigger piece of American household wealth, and that changes the stakes for ordinary investors. When more retirement money sits in equities, market drops can hit household confidence and push policymakers to respond faster.

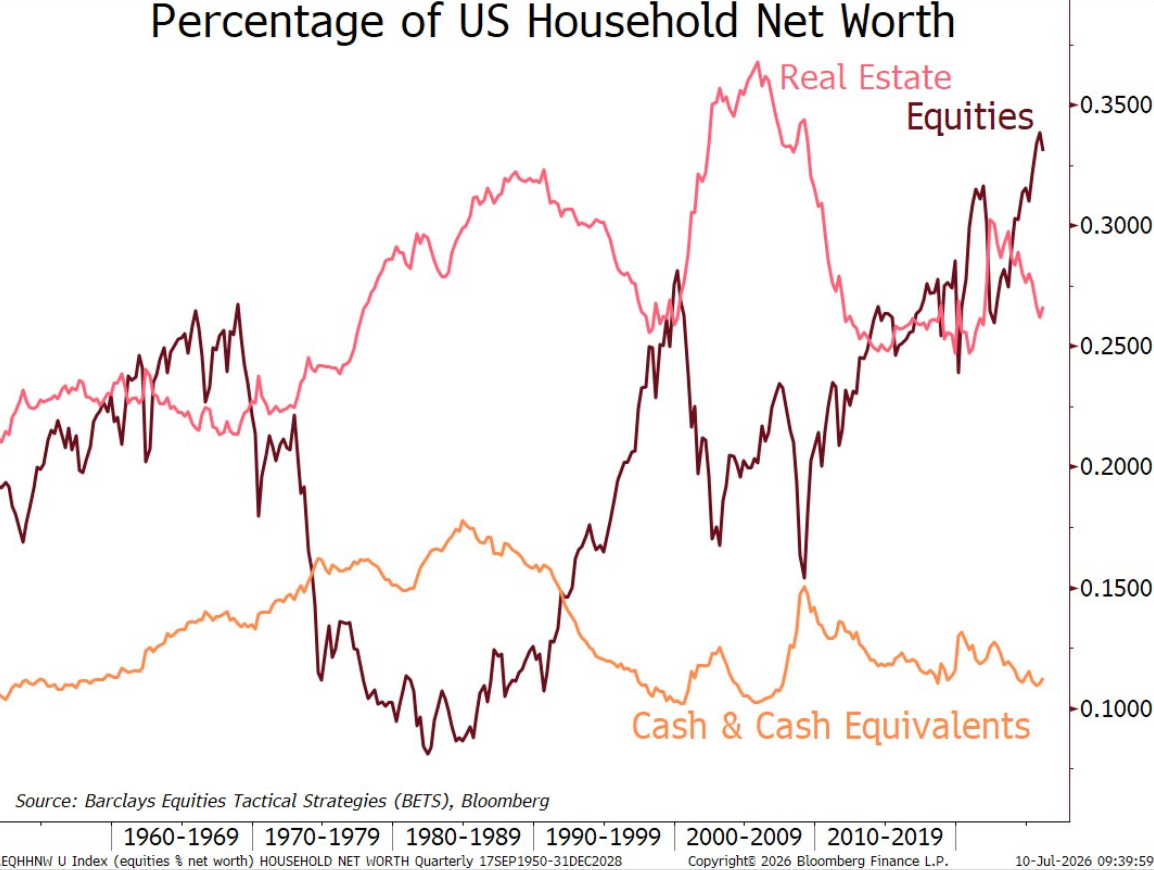

Market commentator Joe Weisenthal shared a chart tracking household allocations across financial assets over time, showing equities ahead by a wide margin. Asset allocation means how investors split their money among categories such as stocks, bonds, cash and other holdings.

The chart has sparked two different readings. A Wealth of Common Sense said the lead for equities could signal stretched valuations or a possible pullback. It also said the shift may reflect a more durable era in which stocks dominate household portfolios.

How stocks became more accessible

For much of the 20th century, many U.S. households had limited exposure to the stock market, according to A Wealth of Common Sense. The blog pointed to lower disposable income before World War II, higher entry barriers, trading costs and limited market knowledge as factors that kept many families away from stocks.

Retirement savings also looked different. Defined benefit pensions, plans that promise retirees a set payment, were more common before defined contribution plans such as 401(k)s became widespread. A Wealth of Common Sense noted that these pensions often felt bond-like to workers because they offered expected payments, while the pension funds themselves were historically more conservative than today’s large retirement investors.

Investor and financial historian Peter Bernstein described that older culture in a 1990s PBS interview cited by A Wealth of Common Sense. Bernstein said that when he entered the business in 1951, many people in the market were older investors shaped by the 1929 crash, and legal rules in some places limited how much trusts or fiduciaries could hold in common stocks.

That structure has changed. A Wealth of Common Sense pointed to individual retirement accounts, 401(k)s, online brokers, zero-commission trading, robo-advisers, target-date funds and platforms such as Robinhood as developments that lowered the barrier to owning stocks. A target-date fund is a diversified retirement fund that automatically adjusts its mix of stocks and bonds as the investor approaches a chosen retirement year.

The policy debate is getting louder

A Wealth of Common Sense argued that the U.S. stock market now carries unusual weight globally, citing the United States’ roughly 4% share of the world’s population, 25% share of global gross domestic product and 65% share of global stock market capitalization. Market capitalization is the total value of listed companies’ shares.

Bloomberg’s Eric Balchunas has raised the question of whether the Federal Reserve could buy stocks in a future financial crisis. According to A Wealth of Common Sense, Balchunas’ case rests on stocks’ role as a retirement vehicle, the size of the U.S. market, broader access to equities, precedents in Japan and China, and investor expectations that the Fed will provide support during crises.

The Federal Reserve has not been reported here as planning such a move. The point is that the idea is now part of the market-policy conversation because equities sit closer to the center of household balance sheets.

A Wealth of Common Sense also tied major policy moments to sharp market moves. It cited the failed 2008 House vote on the $700 billion Troubled Asset Relief Program, followed by an almost 9% stock market decline the next day. It also pointed to the early Covid-era market drop of about 35% within weeks, a later tariff pullback after a 19% slide over days, and energy price spikes as factors that may have influenced government decisions.

The takeaway for retail investors is not a trading call. It is that stock exposure now reaches through retirement accounts, pensions and automatic investing plans, making equity markets a bigger part of the financial system that households and policymakers both have to watch.

This story draws on original reporting from A Wealth of Common Sense.